It seems like every day more and more economic indicators come out in disappointing fashion and the market acts accordingly. The Dow has dropped almost 650 points since August 9th and the S&P has been equally affected. This is indeed significant but now one must asked themselves what to do with their money with such a lack of predictability in the equities market.

You could find yourself asking: is it too late to short particular stocks, because we’ve seen how well the CRM short has worked; is it too soon to call the market oversold, maybe from a resistance level perspective; is it too late to catch the gold train, I personally think so but there is no creditability to that notion; is it too soon to call a top on wheat/agricultural ETFs, who knows, there’s the Russian issue, along with the chance that two hurricanes are going to ravage the eastern seaboard in the near future. We’ve even seen the SIRI perma-bull selling his stake, or at least a large part of it, causing a ruckus in the small community that is SIRI followers.

So what is one to do? You could look at boring fixed-incomes, especially strong corporate bonds or take some risk on international debt offerings. But one could also look at the industry leaders that have been trading strongly within range over the last few weeks of mayhem. And yes, I know that this is going to read just like a dividend aristocrat article (though not all 5 of these meet the criteria), but that’s okay with me because right now they may be the best way to go. With that said we’ll look at the graphs of 5 very strong companies. Not too much analysis will be presented as these companies are very well known and stand on their merits.

McDonald’s MCD – McDonald’s is currently trading around their 52 week high at $73.19, well above their moving averages, and really shows no signs of stopping. Their dividend is at a respectable 3%.

Johnson & Johnson JNJ – J&J has been showing some strong resistance recently. It is mainly held by dividend appreciators who buy up more as the price drops keeping it from falling too far (this is evidenced by the immovable 200 day moving average). Currently priced just below $58 means its yielding 3.7%.

Altria Group MO – People smoke through recessions and Altria is the play to be made in the industry. It trades within a fairly tight range and pays a very nice dividend of 6.2%.

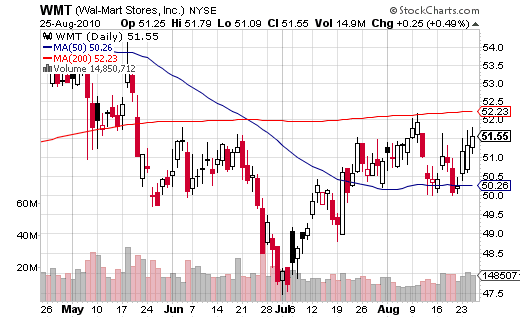

Walmart Stores WMT – Walmart is similar to JNJ in the fact that their 200 day moving average is relatively stable. There has of course been much talk about how one would not have made anything holding Walmart over the last decade, but of course this does not account for their steady dividend, and the fact that their earnings have been increasing over that time is no secret. Walmart is the only stock on this list yielding under 3% and they are currently at 2.4%.

Verizon Communications VZ – Verizon may rub some people the wrong way in that their long term future is nowhere near as certain as the other stocks on this list, but for right now they have been relatively stable, especially after their spinoff of Frontier FTR and latest earnings release. At $29.66 they are yielding 6.5% with room for some growth.

-Jeff